Homeownership vs Renting: The Evolution of Costs and

Income between 2005-2019

Homeownership versus renting a home both have their pros and cons. But which is more fiscally responsible? People often say how much harder it has become to purchase your first home. Housing prices have increased drastically since 2005, primarily due to the boom in 2007. Has income increased at the same rate house prices have? What about rent? Edmonton’s public data will help answer those questions.

Comparing the Increase in Income Versus the Increase in Housing Costs

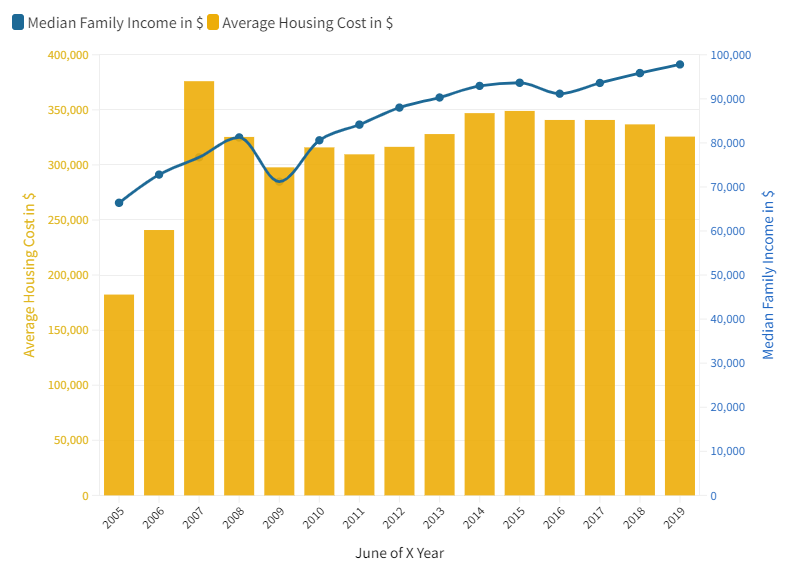

In June of 2005, the median family income in Edmonton was $66,400. Comparatively, the average price of a home was $182,300. June is used for each yearly measurement as this was when housing prices peaked at an all-time high, even to this day. Skipping ahead right to 2007, the median family income had risen to $76,720. At the same time, the average price of a home was $376,000. This is an increase of 106% since 2005. Median family income had only risen by 15.5%, not nearly enough to make up the difference. Jennifer Lamoureux, a mortgage broker and landlord for the last 11 and 10 years, respectively, says that “there’s a saying in the industry. There’s a time to buy, and there’s a time to rent.” June of 2007 would have certainly been a time to rent.

Data gathered from: https://regionaldashboard.alberta.ca/region/edmonton/median-family-income/#/?from=2005&to=2019

;

https://creastats.crea.ca/en-CA/

Edmonton’s public data on median family income only goes up to 2019, so this article will not look at the past two years. However, in 2005 median family income was $66,400. Comparatively, in 2019 median family income was $97,800. That is just over a 47% increase in median family income in Edmonton between the aforementioned years. In June 2019, the average cost of a home was $325,700. That is an increase of nearly 79% compared to June 2005. This data may cause you to think that it has become 32% more expensive to buy a home, but it’s become even more challenging than that.

Over Jennifer Lamoureux’s last 11 years as a mortgage broker, she says that “whenever there are changes to mortgage rules, they usually negatively affect the buyer. Making it harder for renters aspiring to become homeowners to accomplish their goals and making it harder for current homeowners to upgrade to nicer, more expensive homes.” The worst of these changes came in October of 2016 with the implementation of the mortgage stress test. Prior to this stress test, if you got a mortgage with five percent down, you qualified at whatever your interest rate was. For example, if your interest rate was 2.99%, you qualified at 2.99%. However, after the implementation of the stress test, you had to qualify at a rate set by the Bank of Canada. This rate fluctuates typically around four to five percent; however, during the COVID-19 pandemic, they set it at 5.25%. Meaning, if your interest is one percent, you still have to show that you can make payments at 5.25%. This is done to ensure that if interest rates increased to 5.25%, borrowers would be able to make those higher payments in the next term of their mortgage. According to the experienced mortgage broker, “that change really put the brakes on a lot of people’s entry into the buyer’s market.”

Portrait of Jennifer Lamoureux. Credit: Jennifer Lamoureux

Comparing the Increase in Income Versus the Increase in Rent

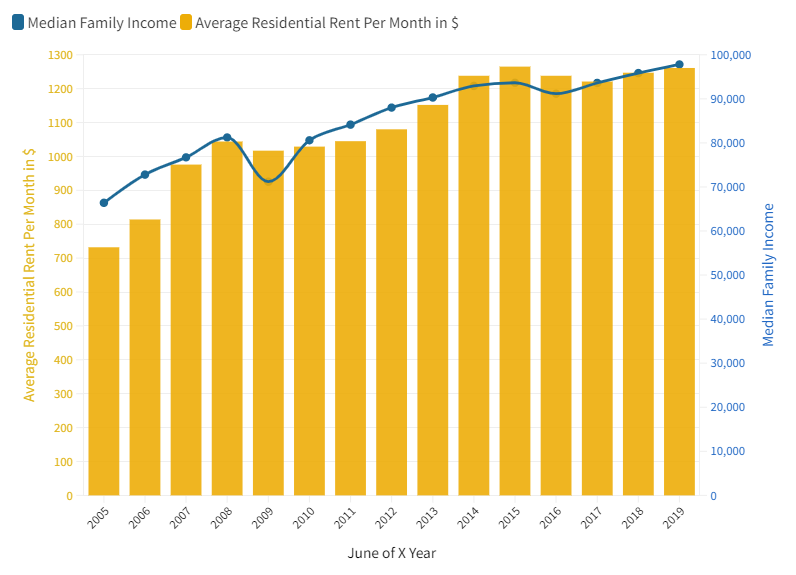

Both average costs of homes and median family income have gone up substantially since June of 2005. Has renting a property in Edmonton made similar increases? In 2005, the average monthly rent of a two-bedroom unit was $732. Comparatively, in 2019 the average cost was $1,261. That is an increase of just over 72%. Close to the rise in the average price of a home, 79%. With median family income only rising 47% in that timeframe, buying and renting a home has become more difficult.

Data gathered from: https://regionaldashboard.alberta.ca/region/edmonton/median-family-income/#/?from=2005&to=2019

https://regionaldashboard.alberta.ca/region/edmonton/average-residential-rent/#/?from=2005&to=2020

But buying a home has become much more difficult than renting, and not by 7% as you may think. Jennifer Lamoureux explains this huge change and how it affected one of her clients. These clients had a $340,000 mortgage on a $450,000 property. Their monthly payment is $2,102.22. The payment to qualify them for that mortgage due to the implementation of the mortgage stress test is $2,723.09. She explains that they would have to make an extra $20,000 to qualify for the same mortgage, 30% higher than they’d have to make before the stress test. She says that in general, “it impacts purchasing power negatively by about 20%.”

The Federal Government of Canada implemented a mortgage stress test to try and control the uncontrollable appreciation occurring in Vancouver and Toronto. The problem is that when the federal government makes a change to mortgage rules, they make them federally instead of regionally. Largely irregular appreciation was not happening in Edmonton, but the purchasing power of individuals in the area was still significantly affected. Jennifer Lamoureux expresses her discontent by saying that “the appreciation largely occurred in those areas through foreign investors that bought the homes outright with cash, meaning there was no mortgage to begin with.”

David Wilber, an e-commerce coordinator, began renting his first property three months ago. After finishing his six-month sublease, he plans to continue renting but change locations. The main factor for the new renter was affordability. He says that “after purchasing a home I could always see myself going back to renting if I had to move around for work constantly.” But adds that he’s “planning to stay in Edmonton his whole life, so continuing to rent probably doesn’t make much sense.”

Portrait of David Wilber. Credit: David Wilber

Is it Better to Rent or Buy?

You can only use 39% of your income towards the cost of owning a home, including 5% extra for other debts that you show. To qualify for the previously mentioned $340,000 mortgage, you would have to show $99,230 gross annual income. Considering the median family income in 2019 was $97,800, and the average cost of a home was $325,700, after taking away the average down payment of five percent or $16,285 on the average home, it seems that the average family income is enough to qualify for a mortgage.

When you insert information about your proposed mortgage, the calculator will tell you how much you would have to pay in rent to be more beneficial than purchasing a home. When inserting all of the average values in Edmonton, the calculator says that when buying an average home, if you can find a rental property for less than $1,064 a month, then “renting is better”. This is on a 25-year mortgage, the maximum term currently allowed in Canada.